Omdia: Global smartphone shipments continue to rise year-on-year for third consecutive quarter in 2Q24

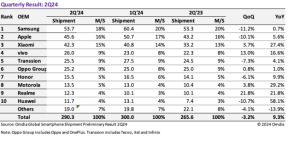

LONDON: According to the latest Omdia smartphone preliminary shipment report, shipments totaled 290.3 million units in 2Q24. Compared to the previous year, this shows a 9.3% rise, following the 11.5% increase in 1Q24 and 8.6% increase in 4Q23. Compared to the previous quarter, this represents a 3.2% fall.

The slow growth indicates the industry is settling to sustainable levels of global shipments, following strong growth between 4Q20 and 3Q21 and decline in 2022. Many OEMs recorded large double-digit year-on-year growth, including Xiaomi, vivo, Motorola, Realme and Huawei, with Apple and Transsion seeing more moderate growth. Transsion, who previously saw triple-digit growth, now has recorded 4.1% growth.

Samsung remains the OEM with the most shipments in 2Q24, with 53.7 million units. This is a 0.7% increase from 2Q23, but an 11.2% fall from 1Q24 due to seasonality. Samsung is facing challenges particularly in the $250-$600 mid-end price segment, where it generates most of its shipments.

Following a fall in the first quarter of the year, Apple recovered to a 5.6% year-on-year growth rate in 2Q24. It recorded 45.6-million-unit shipments, up from 43.2 million in 2Q23, but below the 50.7 million shipped in 1Q24. This second quarter is typically the smallest of the year, so this decline should not be interpreted as Apple struggling. Although Apple’s overall shipments increased year-over-year, shipments in China were found to have decreased compared to the same period last year.

“Recently, the smartphone market has been experiencing accelerated polarization, with the mid-range market shrinking while the proportion of low-end and high-end markets is increasing. Accordingly, while brands with a high proportion of low-end and high-end smartphones are increasing their shipments, brands with a high proportion of mid-end smartphones are struggling,” said Jusy Hong, Senior Research Manager in Omdia’s Smartphone group.

Xiaomi has recorded a large 27.4% increase year-on-year, up from 33.2 million in 2Q23 to 42.3 in 2Q24. This is a marginal 3.7% increase from the previous quarter. Overall, Xiaomi looks to be recovering quickly from a long period of declining market share – from 14.2% in 2021 to 12.6% in 2022 and 2023. Xiaomi had a positive start, capturing 14.1% of shipment share in the first half of 2024.

Vivo rose from sixth to fourth position in the ranking of shipment volume, marking a significant change from the previous quarter. In 2Q24, vivo recorded 26.0 million shipments, up 3 million or 13% from 1Q24 placing them ahead Transsion and Oppo. This is a 16.6% increase from 22.3 million in 2Q23.

Transsion Holdings’ shipments have remained relatively stable rising slightly from 24.5 million in 2Q23 to 25.5 million in 2Q24. This is a decrease from the peak of 30.1 million in 4Q23, indicating that Transsion’s shipments are stabilizing after considerable growth, doubling since 2022. Maintaining these levels long-term will depend on the low-end segment.

“Transsion experienced significant growth in 2023 and is expected to exceed 100 million units shipped for the first time in 2024, as it further establishes its smartphone brands (iTel, Infinix and Tecno) within emerging markets. Much of Transsion’s success is due to a booming market for low-end devices and aggressive expansion into India, Pakistan and Russia.” said Zaker Li, Principal Analyst, Omdia.

Oppo Group recorded 25.2 million shipments in 2Q24, with a 1% up (0.2 million units) from 2Q23. Oppo Group’s shipments, which decreased by 5.7% in the first quarter, returned to growth of 1% in the second quarter. Shipments in the Chinese domestic market decreased, but the increase in overseas shipments led to the increase in overall shipments.

In 2Q24, Honor shipped 15.5 million units, a decrease from 1Q24, which was anticipated. This marks the fourth consecutive quarter of year-on-year growth for Honor, with a 9.9% increase from the 14.1 million shipments in 2Q23.

Motorola maintained its strong performance recording 13.5 million units – a 29.2% increase from 2Q24. This continued growth has propelled Motorola up the smartphone OEM shipment rankings from ninth to eighth place, reclaiming this position from Huawei.

Realme shipments increased to 12.3 million in 2Q24. This represents a 21.8% or 2.2 million increase from the 10.1 recorded in both 1Q24 and 2Q23. The recovery in sales in the Indian market led to an increase in overall shipments.

Despite a slight drop in the rankings, Huawei remains well positioned for growth. In 2Q24, Huawei shipments totaled 11.7 million units, a fall from the previous quarter. However, this figure represents a significant 58.1% increase compared to the same period as last year, it is the highest growth among the top ten smartphone OEMs. This remarkable recovery from its 2021 decline is driven by successive quarterly growth, and the launches of the Mate 60 Pro and the Pura 70 series.