From the Publisher: If globalization is ending, what comes next?

By Eric Miscoll, Publisher EMSNOW

Globalization, as we have known it, is ending. Taking its place appear to be several regional and, in some cases, national supply chains. The primary ones are North America, EMEA, SE Asia, and China. So, what does this mean for the electronics manufacturing industry?

In my recent conversations with executives at EMS companies in EMEA the subject of ‘reshoring’ came up frequently. While the topic has been mentioned increasingly over the past five years, this narrative has clearly now taken hold of the industry’s strategic thinking. Whereas 20 years ago, there was obsessive focus on low cost labor, and the strategy was build your products wherever labor was cheapest, but keep your marketing and sales close to the customer, now there is a decided shift in public and private sentiment in the U.S. and EMEA towards rebuilding regional manufacturing capability.

As a result, regionalization has become a very real trend. Companies are trying to build regional supply chains enabling them to build products in the region for the region. China is still an important manufacturing hub, but mainly for Chinese and other Asian customers. And companies are expanding to Vietnam, Malaysia and Thailand, as well as a serious effort to add India to their footprints in order to effectively serve customers in Asia.

In the Americas, Mexico is seen as the lower cost region for North American customers. The U.S. government passed sweeping legislation to invest in re-establishing the entire semiconductor ecosystem, with cities and states across the country announcing big wins. Private investment in local semiconductor and PCB manufacturing has also increased dramatically. The initial $53 billion Chips Act investment by the U.S. government has reportedly attracted in excess of $462 billion in private funds to the cause, according to my recent interview with David Schild of the PCBAA.

Western European OEMs are building a regional footprint that includes Eastern Europe and Tunisia, as we explained in our recent report. The U.K and the EU have their own legislative initiatives identifying in-country semiconductor manufacturing as a strategic imperative.

So, what changed?

Geopolitical anxiety

In the past, electronics was its own category of products in any nation’s GDP. If your computer failed you could still drive your car, defend your country, control your power grid, and run your hospitals. Not so today. Electronics has infiltrated all aspects of our lives, making national defense departments all over the globe very nervous. Beginning in 2017, the U.S. began imposing tariffs to weaken China’s hold on the global supply chain. As IPC Economist Sean Dubravac explained in a recent video interview by Philip Stoten, tariffs can work, but usually not in the way they were intended. In the case of the U.S. tariffs on China, he says, so far, they have mainly benefitted other countries like Vietnam and Mexico. Nevertheless, these measures have added to the momentum to exit China; although China will undoubtedly remain a major manufacturing center in the future.

Sustainability/energy

Global supply chains produce a lot of carbon emissions. As the planet runs out of easily obtained fossil fuels, attention has turned to how to power it with cleaner, more sustainable energy sources. According to the ISO, “the logistics and transport sector contributes just over a third of global carbon dioxide (CO2) emissions, making it the largest-emitting sector in numerous developed countries. And that share keeps growing. In 2021, the transport sector accounted for 7.7 gigatons (Gt) of CO2 – an increase of 8 % since pandemic measures were lifted. Today, the world’s total annual CO2 emissions are around 35 Gt.” Building products halfway around the globe adds cost, risk and environmental stress.

The people factor

Remember when we all applauded the concept of a ‘service economy’? Now in the U.S., most of the jobs are in ‘FIRE’ industries – i.e. Finance, Insurance, and Real Estate, food service, and healthcare. According to the Brookings Institute, as of 2020, four out of five American workers in the private sector are employed in the service economy, doing everything from delivering care in hospitals and nursing homes to making and serving food to ensuring products make it from ports to store shelves and into consumers’ hands. Universities are not producing as many engineers; marketing and finance degrees have become more popular. This shift is now considered alarming and will need to be addressed much more concertedly to enable the transition.

Speaking Of Transitions

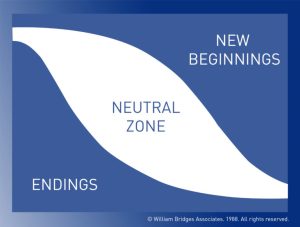

I have always liked William Bridges’ model for transitions. As he would say, ‘It’s not the changes that do you in, it’s the transitions.’ Transitions begin with an ending, and end with a new beginning, and in between is a period of uncertainty he terms the neutral zone.

If manufacturing is shifting to a regional model, this is going to be a big transition. It took decades to establish globalization and its associated global supply chains; and it will take time and focus on this transition to ensure success. According to the Bridges Model, transitions start with an ending. This is paradoxical but true. This first phase of transition begins when people recognize a change, identify what they are losing, and learn how to manage these losses. For business it means a shift from an old model to a new model. Think of the business transition that occurred with the advent of the internet.

The second step of transition comes after letting go: the neutral zone. People go through an in-between time when the old is done or fading, but the new isn’t fully evident and operational yet. It is when the critical psychological realignments and repatternings take place. It is the very core of the transition process. During this time, which can be lengthy, it is important to build temporary structures or bridges towards the next phase – the new beginning.

New beginnings involve new structures, understandings, values, and attitudes. Beginnings are marked by a release of energy in a new direction – they are an expression of a fresh identity. Well-managed transitions allow people to establish new roles with an understanding of their purpose, the part they play, and how to contribute and participate most effectively. The result should be reorientation and renewal.

I believe the EMS industry is in transition, where executives are lessening their focus on cheap labor in favor of a total cost analysis and supply chain security. We are in the neutral zone. This can be an unsettling time, but also a time of tremendous innovation and opportunity. Can the industry use this time to imagine new, more efficient and sustainable ways to make electronic products? Can we use technology like automation and artificial intelligence, not just to save money, or cut labor cost, but to make jobs easier and more attractive to people? Can we re-establish the electronics ecosystems necessary to achieve truly independent regional supply chains? What degree of interdependence will emerge among the various regional supply chains?

Regional supply chains make sense for many reasons. As a wise industry colleague of mine once pointed out: the greatest risk factor when assessing an electronics supply chain is the number of time zones you place between where the order is placed and where it is fulfilled.

Building products closer to the end customer (i.e., local for local) enables shorter, more resilient supply chains that are more responsive to demand signals and able to adapt to the inevitable disruptions that are bound to occur. Electronics manufacturing is a complex activity that craves stability but has become adept at disruption. It should be an interesting transition.

What do you think?